New Guide: From energy to climate management

In cooperation with GUTcert and the registered organization German Corporate Initiative Energy Efficiency (DENEFF), ÖKOTEC publishes a guide that supports companies on their way to climate neutrality.

Will the sustainability report soon be mandatory?

National and EU politicians, companies, industry associations, NGOs, and journalists have been focussing in the recent months on the announced Corporate Sustainability Reporting Directive (CSRD), a new sustainability reporting obligation for companies. We have summarized the most important information for you.

Traditionally, sustainability reports were written by companies on a voluntary basis according to reporting standards such as the Deutsche Nachhaltigkeitskodex (DNK) or the Global Reporting Initiative (GRI). Only listed companies with more than 500 employees were subject to statutory sustainability reporting requirements via the Non-Financial Reporting Directive (NFRD). However, the quality of the sustainability reports fell short of expectations due to a lack of standardization and quality or resilience of the data. The CSRD, like the EU Taxonomy and Sustainable Finance Disclosure Regulation (SFDR), is part of the European Sustainable Finance Framework, which aims to steer investments into sustainable economic activities.

The CSRD is an upgrade of the Non-Financial Reporting Directive, which became German law with the adoption of the CSR Directive Implementation Act (CSR-RUG) by the German Bundestag in 2017. The aim of this update is to expand the number of companies subjects to reporting requirements and to prepare and publish information on sustainability in a consistent and coherent manner. Internal and external stakeholders such as investors, employees, and customers are thus to be offered greater transparency and a more reliable basis for their decision-making process.

Companies will then no longer be required to report only if they are listed but meet two of the following three criteria: either employ more than 250 people and/or generate more than €40 million in sales and/or €20 million in total assets. An estimated 15,000 companies in Germany are affected by this (DNK).

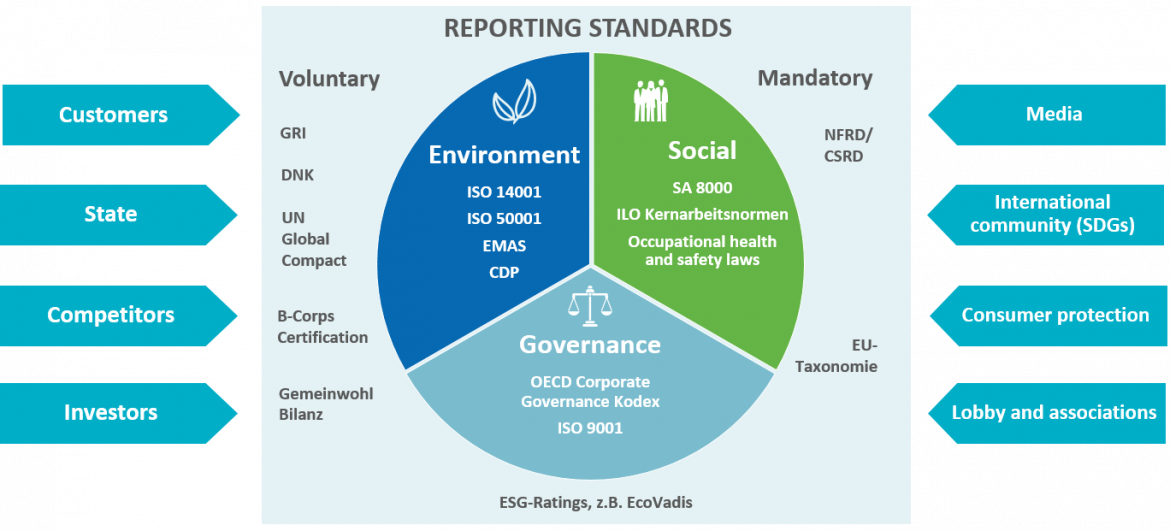

Reporting will be mandatory for all three areas of sustainability management:

In this context, the principle of double materiality should be observed, whereby both the positive and negative effects of the company’s activities on the environment are considered, as well as the opportunities and risks arising for the company as a result of the environment.

Adoption of the law at EU level is planned for mid-2022. However, it is already clear that companies will have to outline their contribution to a sustainable development and to national and European climate protection targets.

On the one hand, this relates to a comprehensive review of the business model and its compliance with the 1.5 degree target. Furthermore, a Corporate Carbon Footprint according to the Greenhouse Gas Protocol, absolute and relative emission reduction targets, planned decarbonization measures, and operational monitoring will be required in order to achieve greater transparency.

The February 2022 European Council proposal recommends staggering the deadlines by company size:

From then on, reporting will take place exclusively in the management report, which must be published alongside the annual financial statements of medium-sized and large corporations and partnerships.

Attention: Even if small and medium-sized enterprises are not subject to reporting requirements in the first step, it can be assumed that they will nevertheless be indirectly affected by the CSRD. Customers and investors who are subject to reporting requirements will increase the demands on cooperation with small and medium-sized enterprises in order to be able to fulfill their own reporting requirements and self-imposed sustainability goals.

On November 10, 2022, the European Parliament adopted the proposed directive with a large majority at first reading. On November 28, the CSRD will be submitted to the European Council. After that, national governments have 18 months to adpot the directive into national law. In November 2022, the European Financial Reporting Advisory Group (EFRAG) plans to publish the revised draft of the European Sustainability Reporting Standards (ESRS) and will submit them to the European Commission. (paragraph updated on: 14.11.2022)

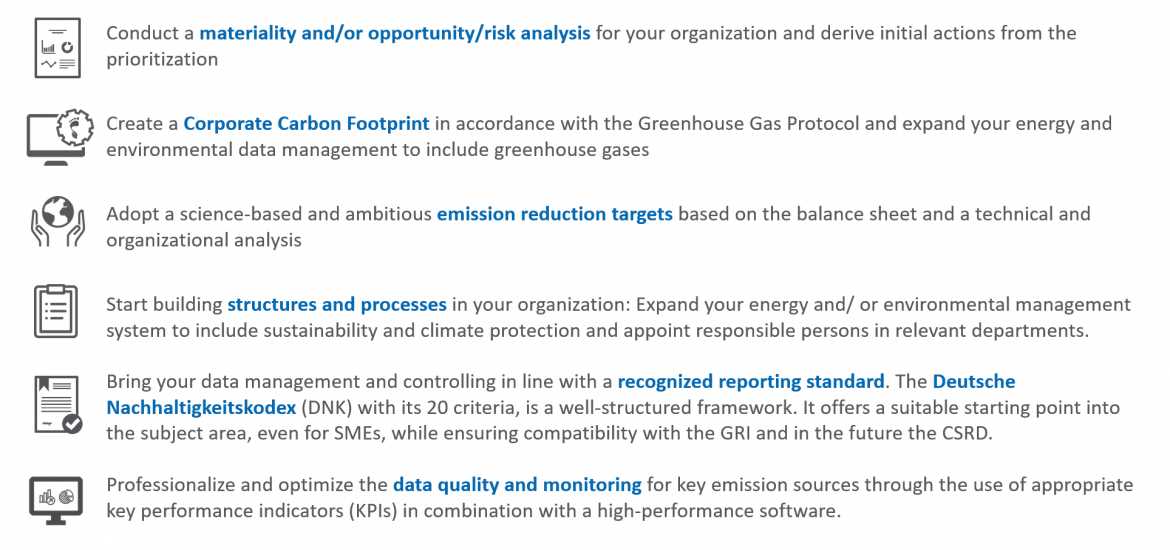

Even if the deadlines are still far in the future, we recommend that you start reporting promptly and initiate appropriate measures. This is why: A CSRD-compliant report requires strategic decisions and many topics have to be coordinated with different departments, which will take time! We have compiled some tips for initial steps and measures:

In cooperation with GUTcert and the registered organization German Corporate Initiative Energy Efficiency (DENEFF), ÖKOTEC publishes a guide that supports companies on their way to climate neutrality.

The new BMWi subsidy “Transformation Concepts” is launched: It supports companies on their way to climate neutrality. They receive a funding rate of 50% for their concept, the maximum funding amount is €80,000.*

By 2030, the CAFEA Group aims to produce coffee as climate-neutrally as possible. In order to achieve this, greenhouse gas emissions are being minimized and the product portfolio is being made more eco-efficient and effective.

Image: Vitalii Vodolazskyi/Shutterstock.com